Justin Kozak

EVP

Key Takeaways

EVP

Update: We’ve released a new whitepaper examining the Cannabis industry. We dive into the insurance landscape, legal climate and how to approach risk management for companies in this sector. You can download the report here!

Plenty of industries are booming nowadays—fintech, on-demand, micromobility, etc. The cannabis industry, however, tops the charts for tremendous growth as well as intense social impact. With so many developments in the last half-decade, success only comes through up-to-date knowledge. When it comes to the cannabis industry, here’s what happened the past year and what to expect in 2020.

Industry Overview

The cannabis industry is a sector focusing on the cannabis plant, which is dried and better known as marijuana or pot. Although it’s typically smoked, there are other ways to use it, such as extracting the plant’s oil, cannabidiol (CBD). Keep in mind that two types of CBD, however, one derived from hemp and the other from the marijuana plant.

Various cultures worldwide have used this plant for medical purposes for thousands of years. In recent decades, though, the use of the cannabis plant has shifted to encompass both medical and recreational intents.

With such a widespread social shift, players in this industry have positioned themselves for success by developing and commercializing marijuana-related therapeutics. Some of the largest and most successful companies in the cannabis sector include:

- Canopy Growth Corp.

- Tilray Inc.

- Aurora Cannabis Inc.

- Scotts Miracle-Gro Co.

- GW Pharmaceuticals

- Namaste

- TILT

Cannabis Year Review: 2019

No one has explained it better than Dylan Summers, Director of Government Affairs at Lazarus Naturals, “It is only a matter of time before the optics of cannabis overall is changed from back-alley-indulgence to a serious resource for supplementing a health-forward lifestyle.”

That said, here’s what happened in the cannabis industry in 2019:

Data Drove the Market

With cannabis-related products coming out of the shadows—as Summers predicted—players can now compile consumer data. What’s more; is that this data points to a massive shift in social perspective. From self-righteous finger shakes to care-free shrugs to open arms, the way people think about cannabis changed significantly in 2019. And the data backs it up.

Cannabis-related Venture Capital Skyrocketed

Experts predicted a tripling of capital in the cannabis industry, and they weren’t wrong. Investors weren’t about to turn a cold shoulder to such ripe potential. Not only did venture capital (VC) increase in 2019, but the number of VP-backed cannabis businesses did, as well.

CBD Spearheaded the Industry

As mentioned, CBD oil is another popular way to use the cannabis plant. The term “CBD gummies” ranked third as the most searched food-related items on Google in 2018. In 2019, CBD was still having its moment in the spotlight with CBD oil available for purchase to help battle depression, anxiety, and chronic pain. Experts predict that this isn’t just a craze; it’s a sustainable health routine.

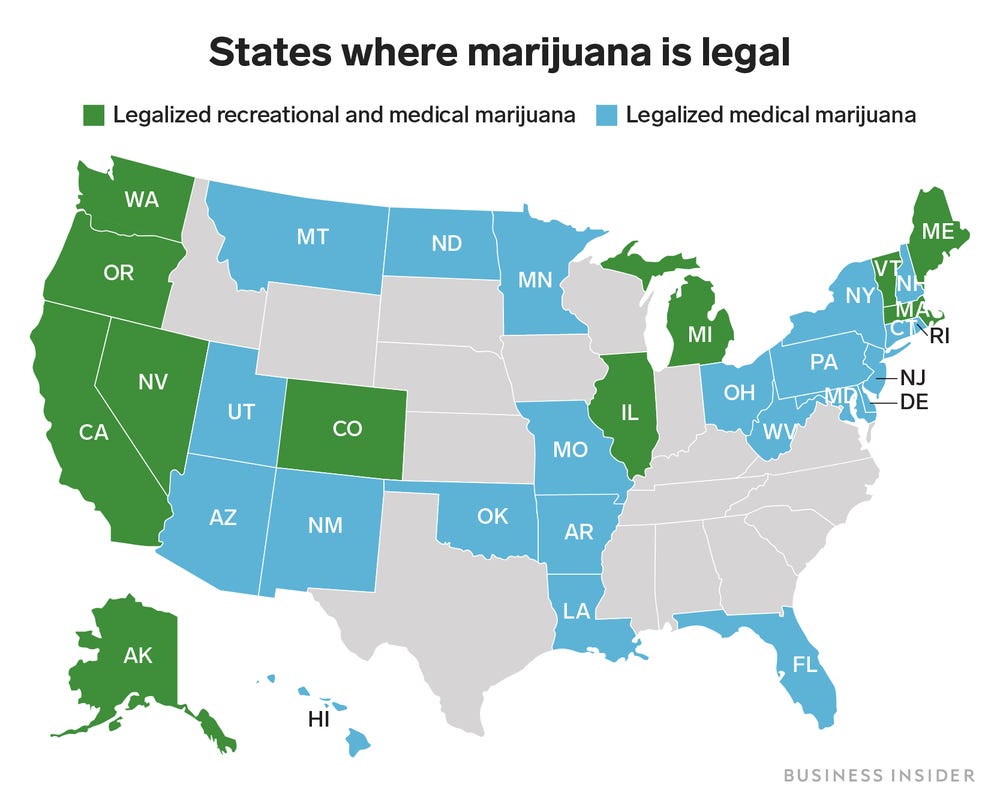

More States Legalized

Medical marijuana is now legal in 33 states, although only 11 others approve of using it for recreational purposes.

Cannabis Trends for 2020

Policy Reform

With the Democrats in control of the House this year, policy reform is a realistic possibility. Plenty of long-awaited bills have been collecting dust over the years, and 2020 might be the year to see them passed.

Big Banks Will Warm Up

Another shift in money flow could take place in 2020. Big banks have been somewhat shy about getting involved with cannabis companies for fear of money laundering. However, the American Bankers’ Association is hoping to bridge the gap between federal and state law by offering clarity to the current muddied relationships.

More Legalization

Of course, mindsets will continue to shift, and more states will legalize recreational marijuana, too. The wheels have been set in motion to legalize in the following states this year:

- Arizona

- Arkansas

- Florida

- Missouri

- New Jersey

- South Dakota

Risks for the Industry

The US has been a reasonably hostile environment for the cannabis industry for many decades—but that’s all changing. Still, this sector faces unique exposures that some industries don’t.

Shareholders

With the industry experiencing massive growth and VC backing much of it, shareholder lawsuits are becoming more prevalent. This trend will likely continue this year, and it will potentially cost the industry a significant amount of money.

For example, Cronos, a Canadian-based company distributing cannabis products, faced a securities class action lawsuit in 2018. In this class action suit, a Cronos shareholder filed the suit against the company and its CEO, Michael Gorenstein alleging misrepresentation of business operations and legally signed contracts.

Banking

Cannabis companies are unable to do business with federally-insured banks because cannabis is still considered a Schedule I drug—drugs that have no accepted medical use and are prone to be abused. Although this unique risk hasn’t stopped the rush of investors interested in the space, it does create complications in financing and funding. However, and as mentioned, passing bills, such as the SAFE Banking Act, might help other big banks to warm up to cannabis more.

Media and People

Much of the US still views the cannabis industry as a risky one. Plus, negative media coverage on the sector only adds fuel to the fire. Battling mindsets, misunderstandings, and misconceptions about hemp-related products make it challenging for industry leaders to move forward worry-free. What’s more; is that social negativity makes getting operational permits from local governments or buying insurance somewhat tricky.

Another significant concern is the workforce in the cannabis companies—or any company, for that matter. Millennials tend to move from job to job more often than other generations, which is creating somewhat of a dilemma for the cannabis industry as there are usually more jobs than applicants.

Insurance Landscape

The cannabis industry works to balance safety, health, and revenue—all while working in the framework of state-specific legislation and being federally illegal. This uncommon situation, coupled with being an emerging industry, has led to unique challenges when it comes to purchasing insurance.

A significant hurdle cannabis companies face on the insurance front is the capability of insurance companies to offer coverage in the space. Many larger, house-hold name insurers are unable and unwilling to provide coverage for these companies due to the federal view of the cannabis plant and its products as a Schedule I drug.

What’s more; is that the insurers themselves are either publicly traded or have restrictions in their reinsurance treaties, which remove this industry from their underwriting appetite. This circumstance has led to a limited market place, creating less competition and thus leading to higher premiums by those insurers who can provide the coverage.

The coverage line that has been affected the most by these challenges is for management liability—particularly for those companies that have US-based operations. D&O coverage, in particular, comes at a higher cost for a similar level of coverage for more widely accepted businesses, as there are only a handful of insurers who can provide comprehensive coverage.

Comprehensive coverage in the space does come at a cost. While there are some cheaper options on the market, many of those include Cannabis specific or regulatory-related exclusions. These exclusions greatly limit how coverage would react in the instance of a claim, leaving companies exposed even though they’ve purchased “coverage.”

On the property and casualty front, an issue many clients experience is in regards to bundling coverage across business operations in multiple states. MSO’s have had to rely heavily on separate policies for each state in which they operate, which can lead to issues ranging from how claims are paid out (i.e. multiple named insureds on multiple policies) to the logistical nightmare of managing upwards of 20+ policies for larger operators. AlphaRoot has been able to help clients navigate this problem, and have partnered with specific carriers who have adapted and started writing across state lines.

Insurance Products

Many industry experts believe that we’ll continue to see class action lawsuits surrounding deceptive business operations. No matter what trends 2020 brings, it’s safe to say that insurance companies have been transforming their products since 1996 when California first legalized cannabis for medical purposes.

Because the industry still carries a stereotype of instability, many carriers only offer key coverages, such as general liability, property liability, and product liability. However, more insurance products are being developed continually, including :

- Manufacturing insurance

- Dispensary insurance

- Building insurance

- Cultivation insurance

- Laboratory insurance

- Transport insurance

Pricing Trends

Cannabis insurance has plenty of unique variables that factor into its overall cost. That said, premiums, coverage, and limits vary among providers. However, some elements that affect rates include:

- Size of the company

- Business operations (fully integrated from seed to sell, plant vs non-plant touching, etc)

- States in which the company operates (is it a Multi-state operations)

- Is there a US presence

- Insurance coverage selection

- Claims history

The nascent cannabis industry lacks the extensive risk data available in more established sectors, making some insurers cautious. This translates to conservative pricing. However, there are specialized insurers who understand the unique risk landscape and can offer coverage solutions for cannabis businesses. By implementing effective ways of managing risk, businesses can demonstrate proactive risk mitigation strategies, potentially leading to more favorable insurance terms.

Founder Shield Predictions

Short-Term Market Contraction and Hardening

AlphaRoot predicts that the cannabis industry—not unlike the rest of the insurance marketplace—will continue its contraction and hardening presented in 2019. Due to claims and regulatory concerns, several markets who previously dipped their toes in the space will and have changed their appetites at the start of 2020. Below are two examples of the changing capacity and underwriting appetite for the cannabis industry:

- The Bermuda marketplace can no longer write risks with a US presence. Along those same lines, the London marketplace remains hesitant to write any cannabis risks regardless of location.

- Depending on operations, the insurance marketplace has had a shifting appetite toward vape-related exposure due to the vape crisis. AlphaRoot has seen many insurers pull back on their ability to offer coverage for vape-related exposures.

Adaptation of Traditional Insurance Products to the Cannabis / Hemp Industry

AlphaRoot has been in contact with several companies looking to offer creative risk solutions for those in the cannabis and hemp spaces. These companies are taking traditional insurance products, such as weather modeling for crop insurance, and tailoring that toward the cannabis space for both indoor and outdoor growers.

Growth of Cannabis Advocacy Groups

AlphaRoot has built unique relationships with industry leaders to bridge the gap of education and insurance in the cannabis space. The National Cannabis Risk Management Association (NCRMA) is one of those groups that look to provide education and risk mitigation strategies for cannabis companies.

Understanding the details of what coverage your company needs can be a confusing process. Founder Shield specializes in knowing the risks your industry faces to make sure you have adequate protection. Feel free to reach out to us, and we’ll walk you through the process of finding the right policy for you.

Want to know more about cannabis insurance? Talk to us! You can contact us at info@foundershield.com or create an account here to get started on a quote.